In celebration of its 50 years, LIA showed thanks to the support received from industry giants IPG Photonics, Coherent, Han’s Lasers and TRUMPF, at the world-famous Thomson Reuters building in Times Square.

The digital screens displayed a prominent message for the commemorative occasion,

“On its 50th Anniversary, LIA would like to thank Coherent, Han’s Laser, IPG Photonics and TRUMPF for its support.”

Complimenting this message was a bold statement below, previewing the future of LIA and its strategy to shape the future of the photonics industry:

“Defining the next 50 years of photonics – LIA.”

Celebrations Continue at ICALEO with Industry Partners

LIA will address the global photonics materials processing landscape at its 37th annual edition of ICALEO. Laser industry professionals from academic and industrial backgrounds will gather at the Rosen Centre Hotel in Orlando, FL, from October 14-18.

This year will see past presidents, board members and corporate members all in attendance celebrating LIA’s 50th year, with many bringing memorabilia to celebrate the occasion.

“LIA’s 50th birthday is a time for us to reflect on our great achievements and contributions in the growth of this industry over the years. It also marks a time for us to be innovative and pave the way to success together, over the next 50 years,” commented Dr. Nathaniel Quick, Executive Director of LIA.

ICALEO annually draws international crowds of attendees and companies, showcasing and discussing the latest in photonics microprocessing, nanomanufacturing and materials processing. Prominent companies in attendance this year will include Beijing JCZ, Coherent, Edgewave, Han’s Laser, IPG Photonics, SPI Lasers and TRUMPF.

The Laser Institute of America (LIA) will examine the photonics materials processing landscape worldwide at its 37th annual edition of the International Congress on Applications of Lasers and Electro-Optics (ICALEO). Laser industry professionals from academic and industrial backgrounds will gather this year at the Rosen Centre Hotel in Orlando, FL, October 14-18. ICALEO annually draws crowds of international attendees and companies, to discuss the latest in photonics microprocessing, nanomanufacturing and materials processing.

LIA’s Executive Director, Dr. Nathaniel Quick, opening for last year’s ICALEO conference. LIA and ICALEO 2018 will focus on photonics materials processing and innovation, in line with the major growth in this sector.

Global Laser Materials Processing Market is a Booming Sector

The global photonics market accounted for USD $548.63 billion in 2017 and is expected to reach $1344.56 billion by 2026, at a CAGR of 10.5% over the forecast period, in Stratistics MRC’s report. The report quotes Coherent, TRUMPF, IPG Photonics and Han’s Lasers, among the key players in the Photonics market, who will be exhibiting at ICALEO.

The global laser materials processing market is expected to reach USD $23 billion by 2025 according to a report by Grand View Research. Fraunhofer Institute for Laser Technology ILT Director and Past President of LIA, Reinhart Poprawe, commented on the unique global trends driving growth in the sector:

“Additive manufacturing ie. Laser Powder Bed Fusion and ultrafast laser applications are probably the two biggest drivers in the near future, for growth in the laser materials processing sector – with quantum technology marked as the next real big application and impact to society.”

Laser Institute of America to Focus on Innovations and Photonics Materials Processing

This year’s ICALEO will feature speeches from prominent past presidents and board members on the history and future of the photonics industry and LIA, in celebration of the institutes’ 50th Anniversary.

LIA’s Executive Director, Dr. Nathaniel Quick said,

“This year, our 50th anniversary, we are revisiting the past achievements and developments LIA has brought to the industry and continues to bring, in developing standards, applications, education, safety and our long standing conferences, to the sector. The future is bright for LIA and our focus is on innovation and commercialisation of new technologies”.

As part of LIA’s new direction, ICALEO 2018 will not only focus on academia, but will give additional emphasis to innovations in the growing photonic material processing sector along with the impact its vendors are making in this innovative market segment. The newly designed vendor showcase will feature thought leadership panels from industry heavy weights IPG Photonics, Coherent, TRUMPF, Han’s Lasers, Edgewave and Beijing JCZ Technology. These panels will accompany industry presentations, a business breakout stream and a vendor networking evening, with invited media partners to cover this milestone week.

The Opening Plenary will feature keynote speakers ranging from Intel Corporation’s Senior Director, Dr. Islam Salama, Luminar Technologies’ Cofounder and former CEO of Open Photonics, Dr. Jason Eichenholz, and Past President of LIA, Dr. Milton Chang.

Registration for ICALEO is open online until October 14, 2018.

GE Global Research Center’s Dr. Marshall Jones will be headlining this year’s Industrial Laser Conference 2018. Held on day three of the International Manufacturing Technology Show, the one-day industry conference is set to take place on the 12 September at McCormick Place, Chicago IL.

A thought-leader in the advancement of laser materials processing and laser device development, Dr. Jones will be at the Industrial Laser Conference to discuss laser applications in the manufacturing process.

“The adoption of laser technology in manufacturing has been steadily growing, evident by the continued annual growth of laser sales globally where Europe has led the way, especially in Germany. Laser technology will continue to displace more conventional manufacturing processes due to it being faster, automatable, and cost effective,” said Jones.

As the Chief Engineer, Dr. Jones joined the GE Global Research Center in 1974 as a mechanical engineer after receiving his M.S and Ph.D. from the University of Massachusetts. His career at GE saw him advance laser materials processing, laser device development and fibre optics to afford him 55 U.S. patents, 57 foreign patents, and over 50 publications. Last year Dr. Jones was inducted into the National Inventors Hall of Fame for his accomplishments.

The Industrial Laser Conference is presented by the Laser Institute of America in partnership with IMTS. The Laser Institute of America will also be hosting the photonics academic and industry ICALEO conference next month.

Nathaniel Quick, Executive Director of the Laser Institute of America stated, “We are looking forward to having a great blend of speakers at the Industrial Lasers Conference, to contribute and ignite industry conversations on industrial laser applications. Our speakers Stan Ream of EWI will be addressing the challenges and constraints to laser applications, and Michael Sharpe of FANUC America will be discussing robotic laser opportunities.”

Dr. Jones will keynote the session titled ‘Case Studies of Industrial Laser Processes Based on Savings and Other Benefits’ at the Industrial Laser Conference. The speaker line-up includes William Adler, Wayne Penn, Ron Schaeffer and more, covering laser applications and laser processing for service providers.

The one-of-a-kind industrial laser applications workshop will have presentations from thought leaders and provide focused industry insights from key companies including IPG Photonics, Alabama Lasers, Stripmatic, EWI, FANUC America and GE.

Registrations for the Industrial Laser Conference is open online until the 12 September 2018.

As a leader and pioneer in developing and commercializing fiber lasers, IPG Photonics’ diverse lines of low, medium, and high-power lasers and amplifiers are displacing traditional technologies in many current applications. Their lasers and amplifiers reach into numerous markets, including materials processing, communications, entertainment, medicine, and biotechnology.

Founded in Russia in 1991 by physicist Valentin P. Gapontsev, Ph.D., IPG originally produced and sold customized glass and crystal lasers, laser components, and wireless temperature meters for hyperthermia. In 1992, the company began to focus on the development of high-power fiber lasers and amplifiers.

IPG landed its first major contract with Itatel, a telecommunications carrier. The company then won a second major contract with DaimlerBenz Aerospace. In 1994, IPG opened a facility in Germany and established its world headquarters in the U.S. in 1998. In 2000, the company invested in new high-capacity production facilities in the U.S. to manufacture its own diode pumps—a major component of its fiber lasers and amplifiers. The company went public in 2006 and is listed on the NASDAQ Global Select Market as IPGP.

With more than 4,000 employees today, IPG has local sales and service in more than 20 countries worldwide. Its three major manufacturing sites are currently located in the U.S., Germany, and Russia.

IPG’s vertically integrated development and manufacturing abilities allow the company to meet customer requirements, accelerate development, manage costs, and improve yields. The company is able to produce all critical components for its lasers and amplifiers, which it markets to OEMs, system integrators, and end users.

Being the first company to industrialize fiber laser technology, IPG has the broadest array of laser products in the industry. This includes high-power fiber lasers up to 100 kW for materials processing, pulsed fiber lasers for marking and engraving, and fiber lasers covering UV, visible, and mid-IR wavelengths.

Having displaced the traditional CO2 and diode-pumped solid-state technologies as the preferred laser tool for industrial material processing, IPG’s high-power CW fiber laser product line is arguably the most important offered by the company. These lasers are used in the cutting, welding, and drilling of metals within various industries ranging from automotive to aerospace to general manufacturing. Much of this product line’s success can be attributed to IPG’s in-house diode fabrication facility, which accounts for cost reductions.

In the next five years, IPG is looking toward the introduction of cost-effective, high-performance, reliable ultra-fast fiber lasers with a pulse duration in the 100 fsec to 10 psec range. With a higher efficiency, this laser advancement will enable smaller air-cooled packages. The company is also looking toward the expansion of fiber laser technology into the MID-IR wavelengths.

The improved reliability and increased efficiency of high-fiber power lasers as an accepted mainstream industrial tool has led to increase in laser adoption in the automotive industry, a trend that is expected to continue with the push to adopt lightweight materials and electric or battery-driven cars. IPG has monitored these shifts in the industry and will continue to be a leading developer in this area.

IPG Photonics has been a member of LIA since 2002. For more information about the company and its products, visit www.ipgphotonics.com.

This was written by Lindsay Weaver Burt in collaboration with IPG Photonics.

These are unsettled times for global manufacturing. Setting aside the normal up and down cycles of manufacturing — a number of global factors — ranging from Brexit concerns, to economic problems in China, turmoil in the mid-East and a new administration in Washington give cause for concern about economic growth prospects.

Trumping (pardon the pun) these concerns is the current status of industrial laser activity in the global manufacturing sector, that seemingly ignoring external effects, are enjoying another growth year (revenues up by more than 10 percent) led by strong double-digit sales of high-power fiber lasers, a surge in excimer laser revenues led by excimer laser silicon of displays and significant rises in uses for ultra-fast pulse lasers.

Fiber lasers at the kilowatt for metal cutting and joining operations, continue to outpace other laser types, representing 41 percent of the total industrial laser revenues in 2016. Fibers’ 12 percent increase came, in part, at the expense of CO2 (-4 percent) and solid-state (-1 percent) lasers. On a percentage basis direct-diode and excimer lasers in our ‘Other’ category enjoyed the largest annual revenue gain (54 percent) in recent years. These lasers have been recording strong gains based on their limited base numbers in several of our last reports. But one application, excimer laser annealing of silicon (FPE) used in mobile phone displays caused one company, Coherent, Inc., to book multiple orders worth several hundred million dollars for system’s to be delivered into 2018.

The overall revenue growth for industrial lasers in 2016, estimated at slightly more than 10 percent, would in reality be more like 4 percent if we deduct the 2016 FPE revenues; leading to fiber lasers inexorable drive to 50 percent of total laser sales. US based IPG Photonics will have a record 2016 as their revenues from fiber lasers for nine months passed $726 million and, at the high end of guidance for the 4th quarter, could be pushing the $1 billion mark (admittedly not all revenues are generated by laser sales).

Joining IPG Photonics near the billion dollar level is Coherent, Inc., whose fiscal year closed in October at a bit more than $857 million, but strong excimer sales at the end of the year should assist them breaking the barrier (not all revenues are industrial laser related). Certainly after their merger with Rofin-Sinar they could be over the $1.5 billion.

Sitting atop the ‘billionaires’ club is industry giant Trumpf Group whose 2015/2016 approached the $2.8 billion mark, of this, laser technology (including some laser systems) alone topped a billion dollars.

The aforementioned is not intended to belittle a fine group of laser companies who also make up the industrial laser market, but it is these Big Three that dominate the news.

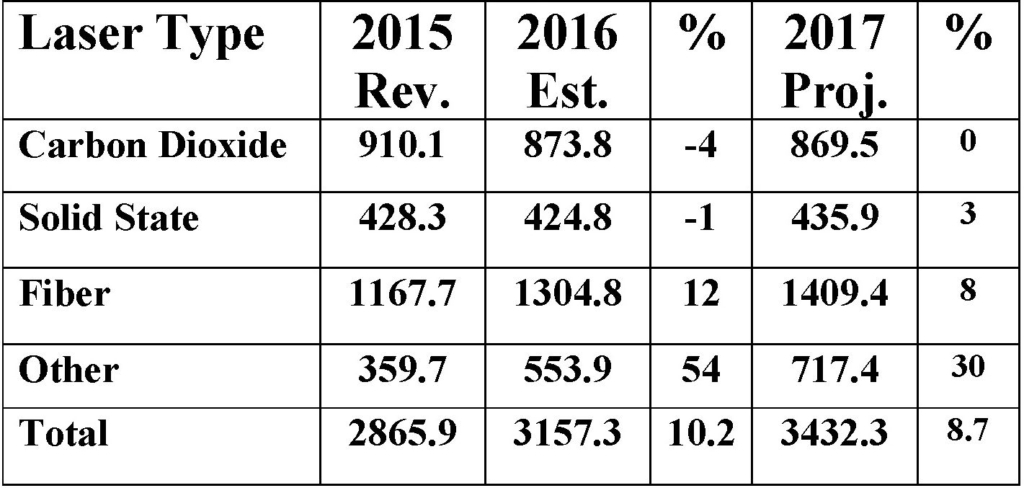

Table 1. Revenues by laser type – Source: Strategies Unlimited

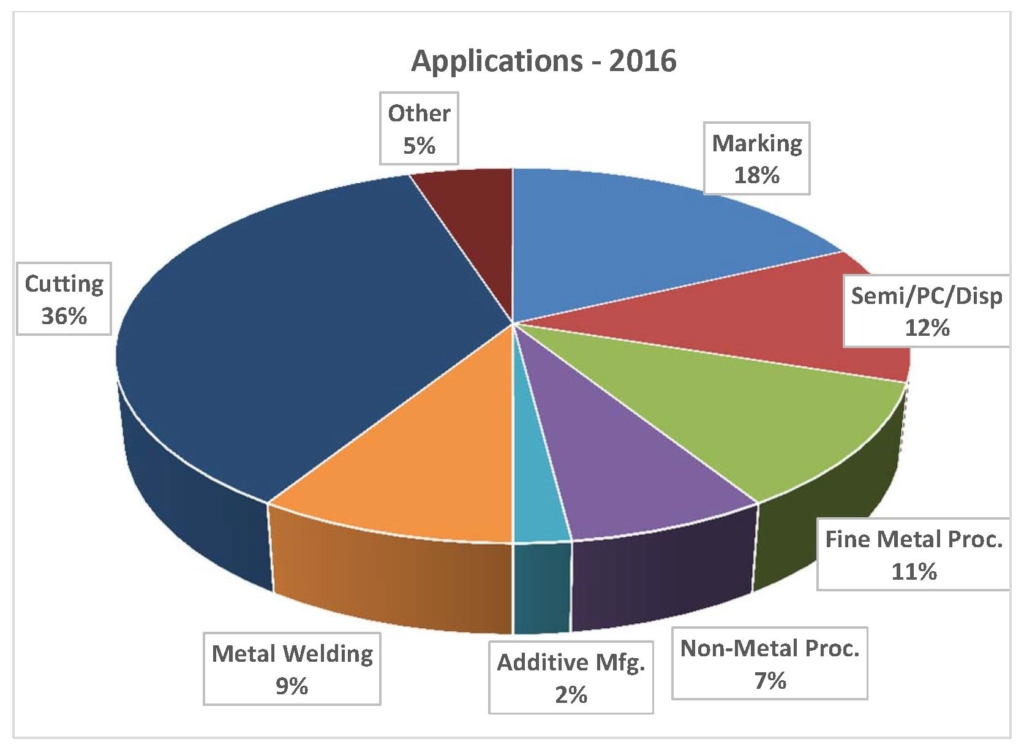

As stated earlier, and shown in the table above, 2016 was another growth year for industrial lasers. In an otherwise moribund global capital equipment market, laser system sales grew in industry sectors that continue to show strength: automotive, aerospace, energy, electronics and communications (smart phones). We divide lasers into three major categories: the first is marking, including engraving, that contributes about 18 percent of all laser revenues and, because this is the most global of all laser markets, traditionally has shown solid growth in all non-recessionary years, continues the trend with a 3.9 percent growth dominated by fiber lasers at 49 percent of the total.

The second category is Micro, which includes all applications using lasers with < 500 W of power, which in 2016 climbed to 35 percent of the total laser market thanks to a 10.2 percent growth in the sector that included display applications requiring excimer lasers. Ultra-fast pulse (UFP) lasers are gaining adherents in the Micro sector and this technology will shore up otherwise decreasing solid-state laser revenues.

The laser category Macro, that includes laser processes requiring more than 500 W of power, is the largest, at 47 percent, of all industrial laser revenues, thanks to fiber lasers which make up 44 percent of all Macro revenues. In 2016, CO2 lasers bore the brunt of fiber laser’s penetration into their largest revenue market, sheet metal cutting, resulting in a 4 percent decline in revenues with an almost 11 percent increase in high-power fiber laser sales. Additive manufacturing demand for more productivity has caused a spurt in higher power CO2 laser demand at the kilowatt level which is factored into the Other category.

Source: Strategies Unlimited

Applications Cutting as an industrial laser application is the most important on two levels: revenues generated and as a user of high-power fiber lasers. Globally over 70 integrators supply flat sheet cutters for metal fabricating. This sector is key among both industrialized and emerging nation economies, therefore its growth prospects are closely tied to a nations GDP. In 2016 global economic growth dipped below 2015 and is expected to expand only slightly in 2017. Thus sheet metal cutting, a key economy indicator, had an off year in terms of growth, with a concomitant softness in high power laser growth to 3.5 percent, which was irregular around the globe.

Fortuitously, expansion in global demand for laser welding (3.4 percent) led by the auto industry and boosted by pipeline and downhole oil pipe welding made up the difference.

Non-metal processing applications in paper converting and fiber reinforced polymers combined with fine metal processing (replacing mechanical fine blanking) to add 5 percent to total market growth. Additive manufacturing, more specifically laser metal deposition, grew 22.1 percent in 2016 spurred by acceptance in the aviation engine industry, with some growth in higher-power lasers accounted for in the Macro category. Both intermediate and high power CO2 and fiber lasers are used depending on material selection. In 2016, other less advanced user industries moved more slowly on acceptance as realization of secondary post-LAM processing required ROI readjustment.

The Future Economic projections for manufacturing in 2017 are a repeat of 2016 with pockets of sluggishness (East Asia, South America and Eastern Europe) continuing. For industrial lasers we are expecting a return to recent annual trends in total market growth with a projected 8.7 percent revenue growth. Marking laser sales are expected to show a decline as unit prices continue to erode mainly in the Asian markets.

Micro laser sales will be a bright light in the revenue picture as FPE laser shipments continue and non-metal processing grows in importance. This category will grow to 38 percent of total revenues.

Sales of laser in the Macro category level off to 47 percent of 2017 total revenues, with continued decreasing revenues in the CO2 segment and a shift into high single digit growth in the fiber laser segment with a more typical 8 percent projection. Solid-state laser (buoyed by UFP lasers) should return to the plus side with a 3 percent growth for 2017. An anticipated shift to high-power direct diodes will pump up the Other category.

David Belforte is Editor-in-Chief of Industrial Laser Solutions.